Figuring out what you need for bridging finance now involves more than looking at one interest rate or just multiplying numbers. In 2026, UK bridging loans will be shaped with more rules. Lenders now look at several things before they let you know how much you need to pay. If you are a property investor or someone who builds homes, you need to know how each part makes up the total cost. This helps you plan your budget and manage risk in a good way.

Bridging loans are short-term tools that help fill gaps in funding. People often use these loans for buying property, fixing up places, or getting something at an auction. They are quick and flexible. The way you pay for them has different layers. It is important to know all the costs so that what seems like a good deal does not turn into a bad one because of hidden fees or plans that do not work out.

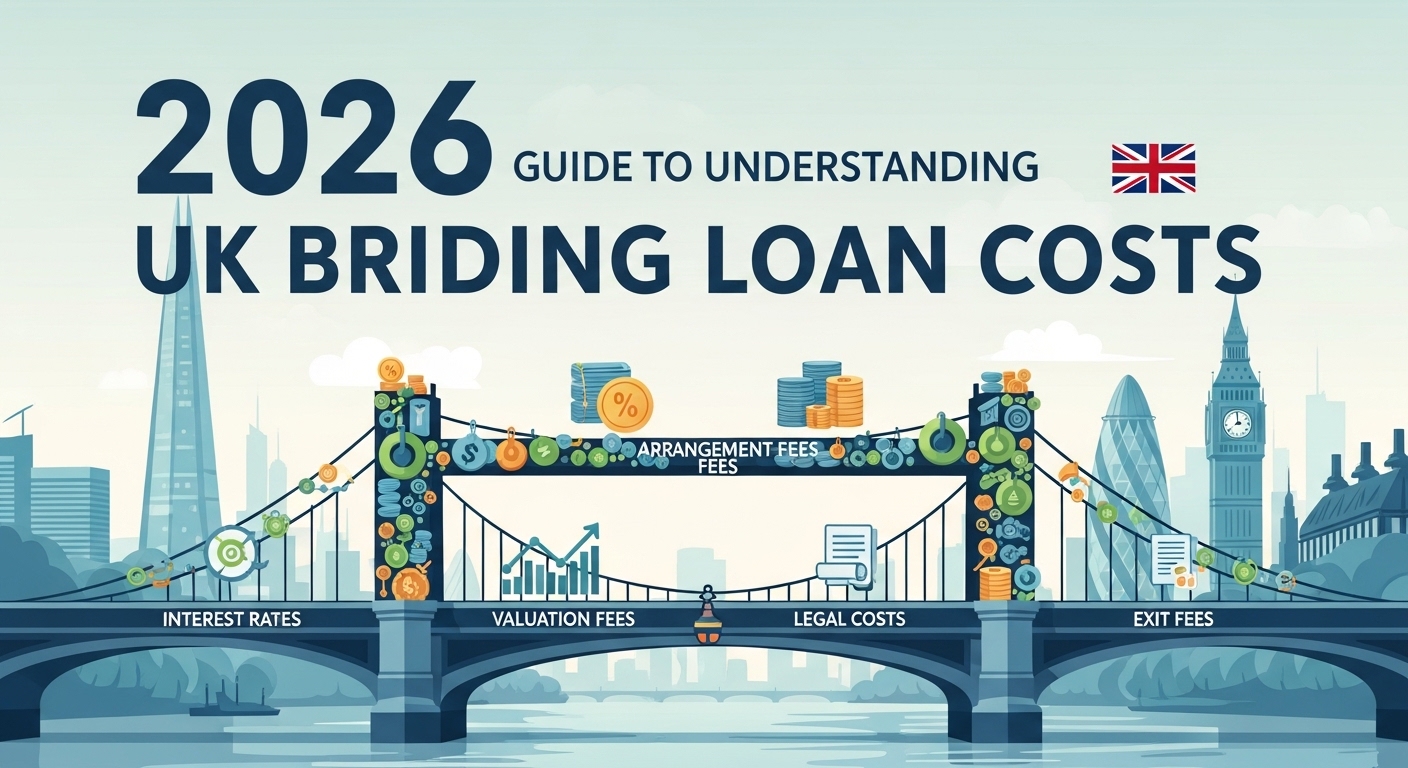

Understanding the Core Components of Bridging Loan Costs

A bridging loan is not priced the same way as a normal mortgage. You do not get one simple interest rate. There is no set repayment plan, either. The real cost comes from many fees put together.

- Arrangement Fees

The lender usually takes an arrangement fee as part of your loan. It is often about 1% to 2% of what you want to borrow. You pay this fee so the lender can set up your loan. Sometimes, you do not have to pay this fee at the start. It can go into your loan, and you pay it off later. While this can help you now, it will make you pay more in the end because of the added interest.

- Interest Rates

Interest on bridging loans is worked out each month instead of each year. In 2026, UK bridging interest rates are usually between 0.44% and 1.5% per month. A bridging cost estimator makes it easy to see how these rates compound—this may look small, but it adds up to a lot when you look at it over a year. Even if the rate goes up or down by just 0.2% each month, it can make a big change to how much you have to pay back after 6 to 12 months.

- Exit Fees

Some lenders may charge an exit fee when the loan ends. This fee is usually about 1% of what you borrowed. The exit fee is there to help the lender when you pay off your loan early or to cover the closing process. Not all lenders do this. If they do, the fee has to be included when you add up what the loan will cost.

Why Using a Bridging Loan Calculator Matters

Manual guesses can miss things, especially when there are many fees and interest added each month. A digital bridging cost estimator helps people who want to invest. You can put in the loan amount, how long you want the loan for, and what your plan is to pay it back. Then, you get a better idea of what you really have to pay back in the end.

The main advantage is that things get clear. Instead of making rough guesses, investors can:

- See how interest builds up each month.

- Check and compare how different lenders set up their loans.

- Try out several situations before you choose.

- Know what happens when you add fees to the amount you borrow.

This way of forecasting helps people have better talks and make better deals. It also stops you from guessing too low about the cash you will need when the job ends or when you move on.

The Impact of Interest Rates on Total Loan Costs

Because bridging finance is short-term, interest adds up fast. A loan with a 0.44% monthly rate over six months costs a lot less than a loan with a 1.5% monthly rate for the same time. But it is not just about the rate. Compounding and extra fees make the gap even bigger.

For example, if you get a £200,000 loan at 0.6% each month for nine months, the total amount you have to pay back will be quite different compared to 1.2%. This is true before you even add on other costs or legal fees. Most people look at how fast they can get the loan, but the interest rate you get is also a key part of the total cost.

It’s important to look at the whole lending package, not just pick the one with the lowest rate. A loan that has a bit higher rate but lower fees can often end up being cheaper than the others.

Loan-to-Value Ratios and Their Influence on Pricing

Loan-to-Value (LTV) ratios show how much you borrow in relation to the value of the property. A 70% LTV means the lender pays 70% of what the asset is worth. The borrower then puts in 30% as a deposit.

Higher LTVs often show a higher risk for those who lend money. So:

- The price to borrow money may go up.

- The setup costs may also get higher.

- The rules to say yes may be harder.

Lower LTVs often get better terms because the lender is at less risk. People with more money in the property may get better rates and quicker answers. When you check costs, change the LTV number in a calculator to see how much money you need and how it will affect you if you can afford it.

Accounting for Legal and Valuation Costs

Two costs people often do not think about enough are legal and valuation fees. You have to pay for these, as they are not optional. These fees can change the total budget for a project in a big way.

Legal Fees: Lenders and borrowers each have their own lawyers. The borrower often must pay for both their own lawyer and the lender’s lawyer. The cost will change based on how tricky the property is and how fast you want to finish the deal.

Valuation Costs: Lenders ask for paid property valuations to find out the right LTV ratios and know their risk. The cost depends on the type of property, where it is, and how soon you need it. Projects for development or places with both homes and businesses often have higher fees for valuation.

If you do not pay attention to these costs, you may run out of money when you finish the project. It is good to include these costs early in your planning. This helps things go well and keeps you from having money problems at the end.

Bringing All Factors Together for Accurate Estimation

Figuring out UK bridging loan costs in 2026 means you need to do more than just look at interest rates. The way arrangement fees, exit fees, monthly interest changes, LTV ratios, legal fees, and valuation charges come together will shape what your final repayment looks like. People who look at all these parts as one, not just on their own, will start to see how good or bad a deal really is.

The use of structured bridging cost estimator tools, comparing lender packages, and testing several money cases is common practice for experienced developers today. When you know the real cost, you do more than stop surprises. You build your power to negotiate, keep your profit safe, and make sure each bridging step fits your long-term plan.

{kind=link}